Divorce requires you to separate a shared financial life, often one account, document, and decision at a time. Retirement assets can be among the most valuable and complicated pieces of that process. They also come with specific rules, tax considerations, deadlines, and paperwork requirements.

Whether you are considering divorce, working through negotiations, or finalizing post-decree details, understanding how retirement accounts are divided can help you make informed decisions and avoid costly mistakes.

This guide explains how retirement assets are identified, valued, and transferred, including the paperwork often required and the tax issues to keep in mind.

Key Takeaways

Dividing retirement accounts in divorce can be technical, emotional, and time-sensitive. A clear understanding of the process can help reduce surprises and protect your long-term financial position.

Here are the main points to understand:

Different accounts follow different rules. A 401(k), pension, IRA, and Roth IRA may each require a different process.

The marital share is usually what gets divided. In many cases, contributions and growth during the marriage are divided, while pre-marriage assets may remain separate.

Employer plans often need a legal order. Many 401(k)s, pensions, and similar plans require a Qualified Domestic Relations Order, or QDRO.

IRAs are handled differently. IRA and Roth IRA divisions typically happen through a transfer incident to divorce, not a QDRO.

Errors can be expensive. Poorly worded orders, missed steps, or direct withdrawals may create taxes, penalties, or delays.

Starting early matters. Draft review by the plan administrator before final court approval can help prevent rejections later.

Understanding these basics gives you a stronger foundation before you begin dividing specific accounts.

Understanding What You Own

Start with a complete inventory. List every retirement account, the plan type, employer or custodian, current balance, and the last four digits of the account number. Collect statements from key dates, including the date of marriage and the date your state or court uses to define the marital period.

If older statements are unavailable, contact the plan administrator or custodian. Many can provide contribution records, account history, or prior statements.

From there, the goal is to separate marital property from separate property. Generally, contributions made during the marriage, along with related growth, are considered marital. Balances that existed before marriage, and possibly the growth tied to those balances, may be separate depending on state law. This tracing process can require payroll records, plan statements, and professional guidance.

The Types of Plans You Might Encounter

Retirement accounts are not divided the same way. Some plans have clear account balances. Others promise future income and require a formula or actuarial calculation.

Understanding the type of plan involved can help you determine the proper paperwork, tax treatment, and timeline.

Defined Contribution Plans

Defined contribution plans include 401(k), 403(b), 457(b), and similar accounts. These plans have individual account balances, which can usually be divided by percentage or dollar amount as of a specific valuation date.

The order may also specify whether the assigned share receives investment gains or losses until the transfer occurs. When divided under a qualified order and rolled into an IRA or eligible employer plan, the transfer is generally not taxable at the time of division.

Defined Benefit Pensions

Traditional pensions work differently because they provide monthly income in retirement rather than a current account balance. A spouse may receive a portion of the future benefit, often based on the years of service that occurred during the marriage.

Important details include when benefits begin, whether early retirement subsidies apply, and whether survivor benefits are included. These decisions should be addressed early because they can affect lifetime income for both parties.

QDROs: What They Are And Why They Matter

Employer-sponsored retirement plans such as many 401(k)s and pensions are generally governed by federal retirement law and often require a Qualified Domestic Relations Order, commonly called a QDRO.

A QDRO directs the plan administrator to divide a retirement account or pension benefit and pay a portion to the former spouse.

Many plans provide sample language, but the order may still need to be customized for plan loans, employer stock, survivor benefits, or other plan-specific features. Whenever possible, ask the administrator to review a draft before it is signed by the court. This step can help avoid delays, rejections, and additional legal costs.

Once the court signs the order, it should be submitted to the plan administrator promptly so the transfer or benefit division can be completed.

IRAs and Roth IRAs

IRAs do not use QDROs. Instead, they are generally divided through a transfer incident to divorce.

The divorce decree should clearly identify the account, state the amount or percentage being transferred, and provide a timeline for completion. The transfer should be made directly between custodians. Avoid withdrawing the funds personally and redepositing them, since that can create tax consequences and possible penalties.

For Roth IRAs, pay close attention to the five-year holding period and contribution basis. Proper documentation helps preserve the account’s tax characteristics for the receiving spouse.

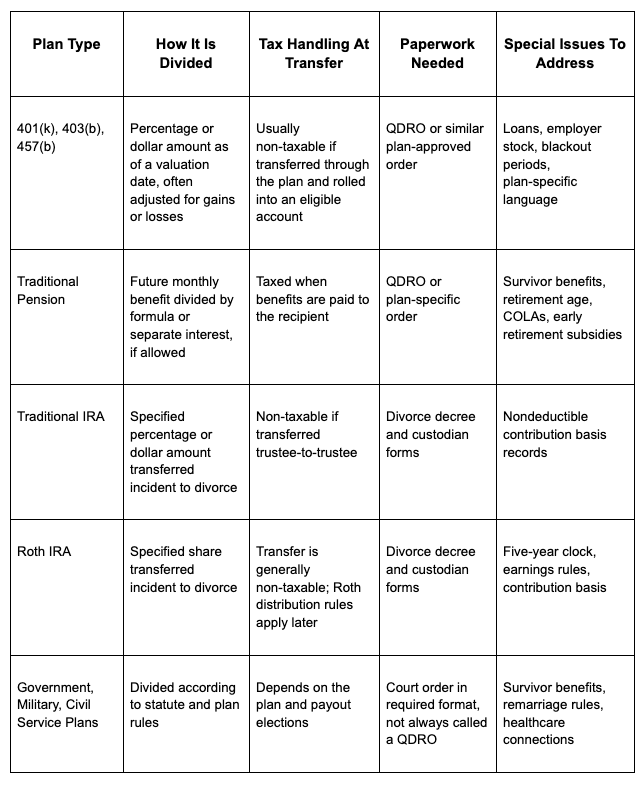

Comparison Table: How Common Plans Are Divided

Different retirement plans require different forms, language, and tax handling. This overview can help clarify what to expect.

Once you know the plan type, you can match the account with the correct process and reduce the chance of delays or tax problems.

Valuation Dates, Growth, And Market Swings

Every division order should include a valuation date. This is the date used to determine the value being divided. Some couples use the separation date, while others use a date closer to the actual transfer.

Plans with daily market pricing, such as 401(k)s, may adjust the assigned share for gains or losses through the transfer date. Pensions may require actuarial valuation or a formula tied to years of service. Confirm the plan’s accepted method before finalizing the language.

Taxes, Withholding, And Rollovers

Tax treatment depends on the type of account and how the transfer is handled.

A QDRO distribution from a 401(k) paid directly in cash is usually taxable as ordinary income.

A direct rollover to an IRA can defer taxation until future withdrawals.

IRA transfers incident to divorce are generally not taxable at transfer, but later withdrawals follow regular IRA tax rules.

Roth IRA distributions depend on qualified distribution rules, including the five-year requirement.

Trustee-to-trustee transfers are often the cleanest way to preserve tax treatment and avoid unnecessary penalties.

Survivor Benefits, Beneficiary Designations, And Insurance

Pensions may require survivor benefit elections so payments continue if the employee spouse dies first. Because survivor benefits can reduce monthly income, they should be negotiated carefully and written directly into the order.

For 401(k)s, IRAs, and similar accounts, update beneficiary designations after divorce. The divorce decree may not automatically override the form on file. In some cases, life insurance may also be used to help protect future income obligations.

Retirement Asset Division Checklist

Documentation matters. Use this checklist to stay organized:

Gather current statements, plan summaries, and model QDRO language.

Confirm the marital period and valuation date.

Decide whether the division will use a percentage or dollar amount.

Specify how gains and losses will be handled.

Address pension survivor benefits and special plan features.

Request plan administrator pre-approval when available.

Use direct custodian-to-custodian transfers.

Confirm completion once the transfer is processed.

A careful paper trail can help prevent confusion and protect both parties.

Common Pitfalls To Avoid

One of the most common mistakes is waiting until after the divorce is finalized to begin the retirement division paperwork. Delays can become more complicated if a spouse changes jobs, a plan merges, or account records become harder to access.

Other issues include vague settlement language, failing to account for taxes, cashing out funds without understanding the consequences, and leaving beneficiary forms unchanged. Each of these mistakes can affect the final outcome.

For Those Already Divorced

If your divorce decree mentioned a retirement account but the transfer was never completed, contact the plan’s QDRO department or custodian. In many cases, a court may still issue a post-divorce order to carry out the original agreement.

If the decree did not mention an account that existed during the marriage, speak with your attorney about possible options. Timing, documentation, and state law will matter.

Working with Your Financial Professional and Other Advisors

Dividing retirement assets involves legal, tax, and financial considerations. Each professional has a different role:

Your attorney helps ensure the order meets legal requirements.

Your financial professional can help evaluate values, tax impact, and long-term planning concerns.

The plan administrator or custodian confirms what the plan will accept.

A QDRO specialist may help draft technical language for employer-sponsored plans.

When these professionals coordinate, the process is often smoother, faster, and less stressful.

Frequently Asked Questions About Dividing Retirement Plans In Divorce

What is the marital portion of a retirement account?

It is generally the contributions and growth that occurred during the marriage. Assets from before the marriage may be separate, depending on state law.

Do we divide by dollar amount or percentage?

Percentages are often more flexible because they can account for market movement between the valuation date and the transfer date.

Do we always need a QDRO?

No. QDROs are typically used for employer-sponsored plans such as 401(k)s and pensions. IRAs and Roth IRAs usually use a transfer incident to divorce.

Will I owe taxes when I receive my share?

Not necessarily. If the division is handled correctly through a QDRO or transfer incident to divorce, the transfer itself may not be taxable. Cash withdrawals are usually taxable.

How long does a QDRO take?

Many plan administrators need several weeks to review and approve a QDRO. Submitting a draft early can help reduce delays.

What if my ex leaves the company before the order is finalized?

The account or benefit may still exist, but administrative changes can complicate the process. Contact the plan administrator quickly.

Can we offset retirement accounts against other assets?

Yes, but compare after-tax values. A pre-tax retirement account is not the same as cash, home equity, or a taxable brokerage account.

Can a QDRO be issued after divorce?

Often, yes. Courts may allow post-judgment QDROs to enforce prior agreements, but acting promptly is important.

What To Remember When Dividing Retirement Assets

Retirement accounts often represent years of saving, planning, and sacrifice. Dividing them during divorce requires more than simply splitting a balance. The process should account for plan rules, taxes, timing, survivor benefits, and your future income needs.

In summary:

Identify every retirement account.

Determine what portion is marital.

Use the correct paperwork for each plan type.

Confirm tax treatment before moving funds.

Keep beneficiary forms and estate documents updated.

Stay involved until every transfer is complete.

A thoughtful process can help you protect your financial foundation and move into the next chapter with greater clarity. If you are navigating divorce and need help understanding how retirement assets may affect your broader financial picture, contact [firm name] for guidance tailored to your situation.