Retirement rarely shows up as one clean finish line. More often, it unfolds through a string of meaningful life transitions that together define this new chapter. From your late fifties into your seventies, shifts in career, family roles, health, and lifestyle can change how you spend your time, how you see yourself, and how your money needs to work.

This guide walks through the big transitions that tend to shape retirement, covering income and tax strategy, healthcare decisions, housing changes, and legacy planning. You’ll also see why the timing and order of these moves can materially affect your options, taxes, and overall sense of control.

Maybe you cut back to part-time, step into a caregiving role, or start thinking differently about what “home” should look like. Meanwhile, choices around Social Security, Medicare, withdrawals, and real estate begin happening in the same window. When these decisions stack up, the sequence matters. A well-timed plan can reduce taxes, manage healthcare costs, and protect long-term flexibility.

If you feel several transitions colliding at once, that’s often a signal to sit down with your financial professional and build a coordinated roadmap.

Recognizing The Life Transitions That Define Retirement

It’s easy to imagine retirement as one major milestone, like leaving a job or selling a home. In reality, these life transitions often arrive in clusters.

Common examples include:

- Moving across state lines can reshape your tax situation and healthcare choices

- Becoming a grandparent may shift your priorities around gifting, travel, or family support

- Receiving a new diagnosis can change insurance needs and everyday spending

None of these decisions happen in a vacuum. Social Security influences taxes and spousal benefits. Medicare timing depends on your work status and your existing coverage. RMDs follow their own schedule, whether you feel ready or not.

So the real question is often not what needs doing, but what should happen first.

Cash Flow Planning For An Evolving Retirement

When the paycheck ends, income becomes something you design rather than receive automatically. A useful structure ties your resources to the kinds of transitions retirees commonly face:

- Immediate cash for regular monthly bills

- Near-term reserves (typically two to three years of spending) to cushion market swings and uneven costs

- Long-term investments positioned for growth and inflation protection

This structure can help you avoid reactive decisions in volatile markets, especially early in retirement, when sequence-of-returns risk can do the most damage. Because IRAs, Roth IRAs, and taxable accounts are treated differently for taxes, the withdrawal order matters too. Pulling from the right accounts at the right time can meaningfully change lifetime tax outcomes as life transitions unfold.

If you’re moving through a major transition, it’s worth reviewing your withdrawal sequence before making any big shifts.

Temporary Tax Advantages In Retirement Years

Certain life transitions create brief but powerful tax openings. For instance, the stretch between leaving work and beginning RMDs often comes with lower reported income. That window can be ideal for partial Roth conversions or harvesting capital gains at more favorable rates.

Life transitions can also be a natural moment to revisit your giving plan and make it more tax-savvy. And if your filing status changes through marriage, divorce, or the loss of a spouse, it’s smart to reassess brackets, withholdings, and benefit coordination.

Short-Term Planning Windows Worth Considering

- Pre-RMD “gap years”: Potential room for Roth conversions or gain harvesting in lower brackets

- Charitable alignment years: A chance to structure gifts that support generosity and tax efficiency

- Coverage or employment changes: A good time to adjust withholdings and estimated payments as income sources shift

Healthcare Transitions That Require Early Planning

Healthcare is one of the biggest, and most time-sensitive, life transitions in retirement. Medicare enrollment windows are strict, and missing them can lead to permanent penalties. If you’ll still be working at 65, confirm whether your employer plan qualifies you to delay enrollment without a cost later.

Long-term care planning deserves early attention as well. Many families eventually face some form of care need, and the cost difference between home care, assisted living, and skilled nursing can be substantial. Treating care as both a financial plan and a practical plan, clarifying wishes, responsibilities, and funding, can reduce stress for loved ones when emotions are high.

If you have a coverage shift or an enrollment window coming up, schedule time with your financial professional to review deadlines, penalties, and the best next steps.

Housing And Family Decisions That Shape Retirement Life

As you approach retirement, housing decisions often rise to the top. Where you live isn’t only a financial choice; it touches comfort, connection, support, and daily rhythm. Many retirees find themselves rethinking not just how they want to live, but where they’ll feel most grounded as priorities and needs change.

Here are a few paths retirees commonly explore:

- Downsizing to cut upkeep and lower expenses

- Staying put while remodeling for accessibility or a simpler layout

- Moving closer to family or to an area with stronger healthcare and social support

- Joining a retirement community or looking into assisted living or long-term care options with graduated levels of support

- Sharing housing with relatives or friends to combine resources, support, and companionship

Family changes, remarriage, divorce, or losing a spouse, can also reshape living arrangements. These transitions often ripple into beneficiary choices, account titling, insurance needs, and estate documents. Handling them thoughtfully, and in the right order, can protect financial stability and reduce stress during sensitive periods.

Building A Portfolio Designed For Today And Tomorrow

Your investment plan should match both where you are now and where you’re going. During life transitions, your ability to take risk often shifts sooner than your comfort level does, which makes a “bucket” approach especially helpful:

- Short-term: Cash for near-term spending

- Mid-term: Bonds or balanced holdings for steadier support

- Long-term: Growth assets for later-life goals

Asset location and tax-aware rebalancing matter during these transitions, too. Keeping tax-efficient holdings in the right accounts, and using withdrawals or contributions to rebalance, can improve results without excessive trading.

How To Stay Disciplined When Life Transitions Hit

Even with a strong structure, headlines or sudden transitions can tempt you to react. These anchors help keep decisions steady as circumstances evolve:

- Purpose-built buckets: Spending, stability, and growth aligned to time horizons

- Tax-location discipline: Matching asset types with account types

- Measured rebalancing: Using cash flow to adjust instead of trading based on fear or hype

If you’re thinking about portfolio changes because of a life transition, connect with your financial professional to confirm how timing, cash needs, and taxes fit your longer-term plan.

Keeping Estate Plans Current Through Life Transitions

One task that’s easy to overlook during or after a life transition is document upkeep. Wills, powers of attorney, and healthcare directives should be reviewed periodically, especially after marriage, divorce, relocation, or welcoming a new grandchild. Beneficiary designations and account titling need to reflect your current intent across IRAs, employer plans, and transfer-on-death accounts.

Your digital estate also belongs in this conversation. Keep a secure record of device access, passwords, and key document locations to make future administration smoother. If it’s been a while since you reviewed these pieces, schedule a meeting with your financial professional to coordinate updates across your legal and financial landscape.

Common Planning Missteps During Life Transitions

When life transitions overlap, it’s easy for things to slip. Some frequent missteps include:

- Missing Medicare or Social Security deadlines while juggling competing life transitions

- Drawing from accounts in a tax-inefficient order

- Forgetting to update beneficiaries after a major life change

- Adjusting investments based on news cycles instead of planning logic

- Skipping paperwork tied to caregiving, property transfers, or new responsibilities

Frequently Asked Questions About Life Transitions Near Retirement

As life transitions stack up near retirement, the same practical questions tend to surface for many households. The answers below address the decisions people most often face, and highlight how timing and coordination can shape better outcomes.

How do life transitions affect when to claim Social Security?

Delaying can raise your benefit; claiming earlier can increase flexibility. The right choice depends on health, spousal planning, and other income sources.

During life transitions, which accounts should be tapped first?

Many households mix taxable, tax-deferred, and Roth withdrawals to manage tax brackets and preserve flexibility as life transitions continue.

Do life transitions change Medicare choices if employment continues past 65?

Often, yes. Some employer plans allow delayed enrollment, but not all qualify. Confirming eligibility before deferring helps avoid penalties.

How do life transitions influence charitable giving?

Coordinating gifts with a tax plan, via cash, appreciated assets, or IRA distributions, can improve both timing and impact.

What documents should be updated during major life transitions?

At minimum, revisit your will, powers of attorney, healthcare directives, and every beneficiary designation after a significant personal or financial change.

Can life transitions create a window for Roth conversions?

Yes. The pre-RMD years can offer more controlled tax brackets for partial conversions, especially after leaving full-time work.

Do life transitions affect HSA strategy?

They can. Medicare enrollment ends HSA contributions, and late enrollment may be retroactive, potentially turning recent contributions into excess. Timing needs careful coordination.

How do life transitions impact downsizing or relocation?

Beyond purchase price, consider property taxes, access to care, proximity to family, and the community network that supports everyday life.

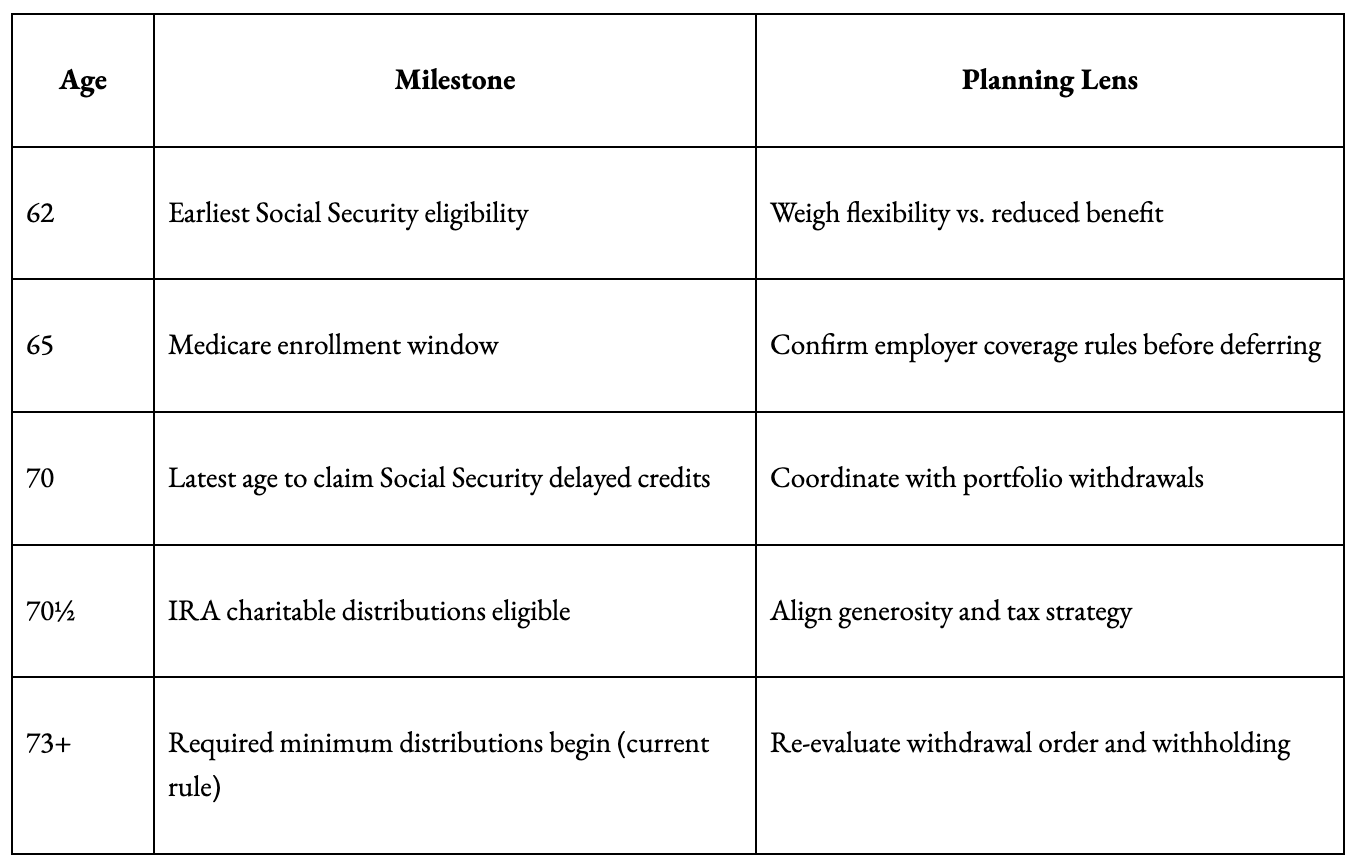

Ages and Turning Points to Plan Around

The Bottom Line: Coordinating Life Transitions With Confidence

Approaching retirement in a thoughtful sequence can change everything, aligning cash flow to timing, making the most of tax windows, coordinating healthcare and housing moves, updating documents, and letting investments evolve alongside your goals. Each step adds structure and direction as you move through change.

If you’re entering this phase, or already navigating several transitions at once, reach out to the office to schedule a meeting. Together, we can clarify your priorities, decide what comes first, and build a plan that keeps your retirement years organized, intentional, and moving forward.