Many executives and highly compensated employees approach retirement with a concentrated stock position, meaning one company’s shares make up a meaningful portion of their net worth or investable assets. If that describes you, your concentrated position may have been built gradually through restricted stock, stock options, employee stock purchase plans, deferred compensation, long-term ownership, or years of holding shares in a company you helped grow.

As retirement gets closer, the planning issue changes. The question is no longer only how the stock helped build wealth, but how it affects liquidity, withdrawal flexibility, portfolio balance, and the timing of retirement income. Managing company stock before retirement means deciding how much single-stock exposure still fits once earned income is winding down and your portfolio may need to support the next phase of life.

Key Takeaways

Managing a concentrated stock position near retirement is less about making a single market call and more about coordinating risk, timing, and cash flow. A thoughtful framework can help you evaluate diversification strategies without losing sight of your broader retirement plan.

Concentrated stock risk can become more meaningful as earned income nears an end.

Diversification can help separate near-term retirement funding from long-term growth.

Risk management includes liquidity, withdrawal timing, tax awareness, and portfolio balance.

Executive equity compensation can link your income, career, and net worth to one company.

A strong strategy weighs tradeoffs rather than treating diversification as automatic or simple.

Your company stock may still have an important role in your financial life. The planning question is how large that role should be when retirement income, spending needs, and portfolio resilience move to the center of the conversation.

Why Concentrated Stock Risk Can Matter More as Retirement Approaches

A concentrated stock position can be a sign of professional success. During your working years, holding company stock may have helped you participate in the growth of a business you know well. Near retirement, the same position carries a different planning weight because your portfolio may soon need to help replace your paycheck.

That shift matters even if you still believe in the company. Concentration risk is not only a question of confidence in the business. It is also a question of timing, liquidity, and how much of your future lifestyle depends on one stock performing well at the right time.

During accumulation, concentration may not feel like a pressing concern because it can build wealth around a familiar asset. During the retirement transition, however, concentration can pose more of a potential risk because the portfolio has new jobs to do rather than simply growing. In retirement, your portfolio may need to fund spending, preserve flexibility, support charitable goals, cover taxes, and remain invested for future growth.

Why Can Executive Equity Compensation Increase Single-Stock Risk?

For executives, company exposure can reach beyond shares held in an investment account. Salary, bonus, unvested equity, deferred compensation, career timing, and future benefits may all be connected to the same employer.

That overlap does not make the stock inappropriate. It does mean the position should be viewed as part of your complete financial picture. If company performance affects both income and assets, your retirement plan may be carrying more single-company risk than it appears to at first glance.

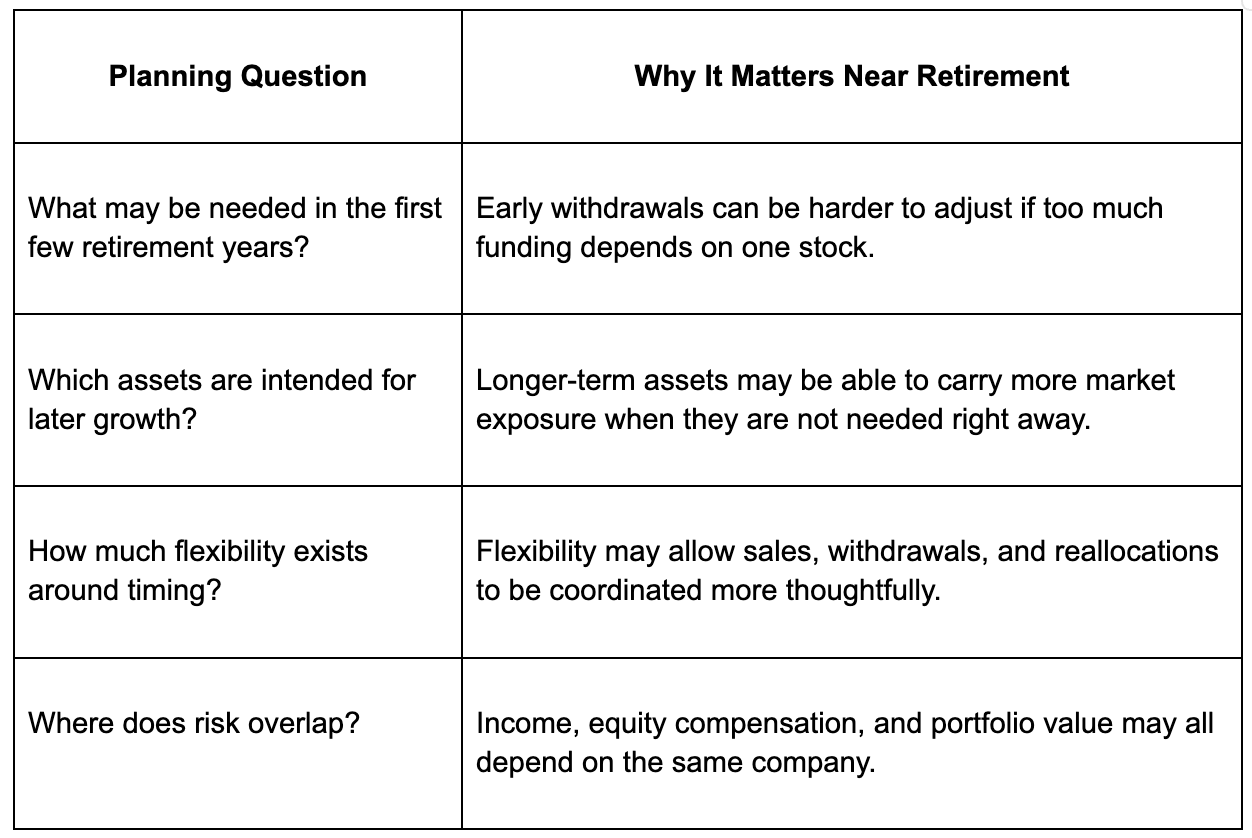

How Concentrated Stock Can Affect Retirement Funding, Liquidity, and Timing

Investment risk near retirement is not only about price movement. It is about what assets are available when you need them to support the life you have planned.

A concentrated stock position may look strong on paper but still create tension if a large share of your retirement spending depends on selling shares during a weak market, a restricted trading window, or a year when other tax-sensitive decisions are also in play. Diversification can help make wealth more usable by matching different assets to different needs.

Matching Assets to Retirement Spending Needs

A retirement funding lens helps separate your wealth into different roles. Some dollars may need to be available soon. Some may be positioned for later spending. Some may be intended for long-term growth or legacy goals.

Once those roles are clear, concentrated stock risk management becomes more practical and less reactive. The conversation moves away from a simple hold-or-sell decision and toward a better question: how much of your future retirement spending should depend on one company’s stock?

Diversification Strategies For Concentrated Stock Positions Can Be Gradual And Coordinated

Diversification is often discussed as though it means selling everything at once. For many executives, the conversation is more nuanced. Diversification strategies for concentrated stock positions can be staged, coordinated, and aligned with your retirement timeline.

Broad strategy categories may include:

Gradual diversification over time, using a schedule that reduces exposure in measured steps.

Partial de-risking, where a portion of the position is reallocated while some company stock is retained.

Liquidity-based planning, where shares are used to support specific near-term retirement needs.

Portfolio rebuilding, where proceeds are invested across a broader mix of assets tied to income, growth, and risk tolerance.

Event-based coordination, where vesting, retirement dates, major expenses, and tax planning conversations shape timing.

None of these paths is automatically right. Each involves tradeoffs around taxes, market exposure, liquidity, opportunity cost, and the role company stock still plays in your financial life. For executives with complex equity compensation, diversification should be considered alongside the full picture, including cash flow, estate goals, charitable intent, and the desired retirement timeline.

If you are evaluating how to diversify a concentrated stock position, contact the office to talk through how the position fits into your broader retirement funding plan. The conversation is not simply about what the stock may do next. It is about how your overall plan supports the retirement season ahead.

What Should Executives Consider Before Diversifying Company Stock?

A good diversification decision rarely feels obvious in the moment. Company stock can represent years of leadership, loyalty, and belief in the organization. That history matters, but it should be weighed alongside the practical demands of retirement.

Keeping shares may preserve future upside and personal alignment with the company. Reducing exposure may improve liquidity and lower dependence on a single stock. Selling in stages can create a more balanced approach, but it still requires discipline, coordination, and a clear purpose for the proceeds, within the broader plan.

How Much Retirement Spending Depends on This Stock?

If the stock will be needed to fund near-term withdrawals, its role is different from a position intended primarily for long-term appreciation or legacy planning. A position that supports lifestyle spending needs a different level of scrutiny than one set aside for future optionality.

How Much Risk Is Already Tied to the Company?

Your company exposure may be larger than the brokerage statement suggests. Salary, deferred compensation, unvested awards, pension-like benefits, and company stock can all point in the same direction. Seeing those pieces together can clarify your real exposure.

What Would Diversification Make Possible?

Diversification can do more than reduce volatility. It may create cash reserves, support early retirement years, fund charitable plans, or reduce the need to sell shares under pressure. The value is not only in owning more investments. It is in giving the plan more ways to work.

What Tradeoffs Are Acceptable?

Reducing concentration may involve taxes or giving up some future upside. Holding concentration may preserve upside but leave the retirement plan more dependent on one company’s performance. The better decision is the one that fits your plan, not the one that looks best in isolation.

How Can Concentrated Wealth Become a More Retirement-Ready Portfolio?

A concentrated stock position becomes easier to evaluate when it is viewed through the retirement plan rather than as a stand-alone investment decision. The planning work is to move from concentrated wealth to coordinated wealth.

Assign A Clear Role To Each Part Of The Portfolio

The planning work is to move from concentrated wealth to coordinated wealth. That does not require eliminating every share of company stock. It does require understanding what role the position should play once retirement income, liquidity, and long-term portfolio balance are part of the same conversation.

A retirement-ready portfolio often has clearer assignments. Some assets support near-term spending. Some provide stability and flexibility. Others are positioned for growth over longer periods. Your company stock can be evaluated against those jobs rather than treated as a separate decision.

Coordinate Diversification Timing With The Retirement Plan

The pace of concentrated position diversification should reflect your retirement date, withdrawal needs, tax considerations, trading restrictions, and the amount of risk the broader plan can reasonably carry. Planning may also involve coordination with your CPA or attorney, particularly when equity compensation, estate planning, or charitable giving is involved.

The purpose is not to remove uncertainty. It is to create a plan that is easier to live with because the stock position, retirement funding, and portfolio construction are working from the same map.

Frequently Asked Questions About Managing a Concentrated Stock Position Before Retirement

These questions come up often for executives and highly compensated employees approaching retirement with meaningful company stock. The answers are general and should be considered within the context of a broader financial plan.

How much concentration risk is too much near retirement?

There is no universal threshold that applies to every household. The right level depends on your retirement spending needs, other assets, time horizon, tax considerations, and how much income or wealth is already tied to the employer.

Why does concentrated stock become more important to address before retirement?

The closer retirement gets, the fewer working years may be available to recover from a major decline. Your portfolio may also need to support withdrawals, making liquidity and timing more important than they were during accumulation.

Is diversification always the right move for executives with large company stock positions?

Diversification is a planning tool, not a blanket rule. You may retain a portion of company stock for long-term growth, legacy goals, or personal preference while still reducing exposure enough to support retirement flexibility.

Can retirement funding be affected even if the stock has performed well for years?

Yes. Strong past performance can increase the size of the position and make the retirement plan more dependent on one stock. A successful company stock position can still create funding pressure if too much future spending depends on its value at a specific time.

What should be considered before reducing a concentrated position?

Key considerations include liquidity needs, retirement timing, tax impact, vesting schedules, trading restrictions, portfolio balance, and coordination with other advisors. The decision should be evaluated before any specific transaction is chosen.

How does company stock fit into a broader retirement income plan?

Company stock can support retirement goals when its role is clearly defined. It may be a growth asset, a future liquidity source, part of a legacy strategy, or some combination of those roles. The important step is making sure it does not carry more responsibility than the overall plan can support.

How to Align Company Stock With Your Retirement Plan

Managing concentrated company stock before retirement means evaluating single-stock risk, diversification strategies, liquidity, timing, and retirement funding together. A concentrated stock position can remain an important asset, but your plan should clarify how much exposure fits, which dollars may be needed soon, and how the portfolio can support flexibility through the retirement transition. To turn a complex company stock position into a coordinated retirement strategy, contact the office to schedule a meeting.