Legacy is more than what heirs receive; it is the way decisions get made when conditions change. The most durable plans combine values, governance, and tax-aware cash flow so wealth supports purpose during calm markets and during turbulence. With a clear mission, aligned documents, and practiced roles, families gain direction when questions arise and confidence when choices must be made.

This guide turns complex legacy planning into practical steps that fit real life. It outlines the four pillars that carry a plan across generations, shows how trusts and cash-flow design can preserve options, and offers tools for preparing heirs without fostering dependency. If a tailored walkthrough would help, contact the office to organize next steps and coordinate with legal and tax professionals.

Key Takeaways

A durable legacy is more than what heirs receive; it is how decisions get made when conditions change. Use purpose, structure, and clear governance to turn wealth into outcomes that last.

- Define the mission: identify who benefits, non-negotiables, decision rights, and how disagreements are resolved.

- Align the plumbing: titling, beneficiaries, and trust terms should match the mission and stay current with tax law.

- Fund the plan tax-smart: sequence withdrawals, consider QCDs and Roth conversions, and place assets intentionally.

- Write the rules: a family meeting rhythm, letters of wishes, and an Investment Policy Statement keep actions consistent.

- Develop people: teach skills, create accountability, and introduce responsibility in stages before it is needed.

- Coordinate advisors: ask for joint sessions with legal and tax professionals to stress-test provisions and documents.

Bottom line: an enduring legacy blends purpose with practical design, then stays adaptive through periodic reviews. When you are ready to translate ideas into action, contact the office.

What Legacy Really Means In Retirement

Inheritance is only the surface. Legacy in retirement is a living framework that shapes decisions when circumstances shift. It captures the values, stories, and priorities that explain why assets exist and how they should serve the family’s well-being. When that intent is explicit, trustees and heirs can act with consistency during calm periods and with steadiness when volatility shows up.

From Account Balances To Family Outcomes

Large balances do not automatically create good outcomes; clarity, coordination, and repeatable processes do. Begin with a one-page legacy statement that identifies beneficiaries, non-negotiables, the latitude heirs have, and a simple process for resolving disagreements. Include who decides what, what success looks like in daily life, and how to escalate issues that fall outside the rules.

Revisit the statement each year to reflect new laws, family changes, and lessons learned. Use the review to align titling and beneficiaries, refresh trustee guidance, and confirm that investment and withdrawal rules still fit the mission. Over time this cadence turns wealth from a set of accounts into a system that funds education, supports independence, and sustains family purpose.

The Four Enduring Legacy Pillars

An enduring legacy does not happen by accident; it is built with a simple, repeatable framework that families can follow in calm markets and in turmoil. The four pillars below convert broad intentions into day-to-day guidance that travels with assets and across generations. Read them as a checklist of decisions to make, documents to align, and habits to practice. Start with a draft that is good enough, then refine as roles, laws, and family needs evolve.

- Governance. Craft a mission statement in plain language, set meeting rhythms, and document decision rights.

- Structures. Align titling, beneficiaries, and trusts with protections and intent.

- Financial engines. Clarify cash-flow sources, rebalancing rules, and reserves.

- Human capital. Prepare successors with skills, mentorship, and accountability so distributions support growth.

After reviewing the pillars, translate them into actions with dates, owners, and a short agenda for your next family or advisor meeting. Keep the language plain so successors can follow it without guesswork, and pair each principle with one small step you will take this quarter.

Revisit the framework annually to confirm it still fits your goals and circumstances. With that rhythm in place, the next section will show how to link these pillars to tax-aware cash flow and durable investment rules.

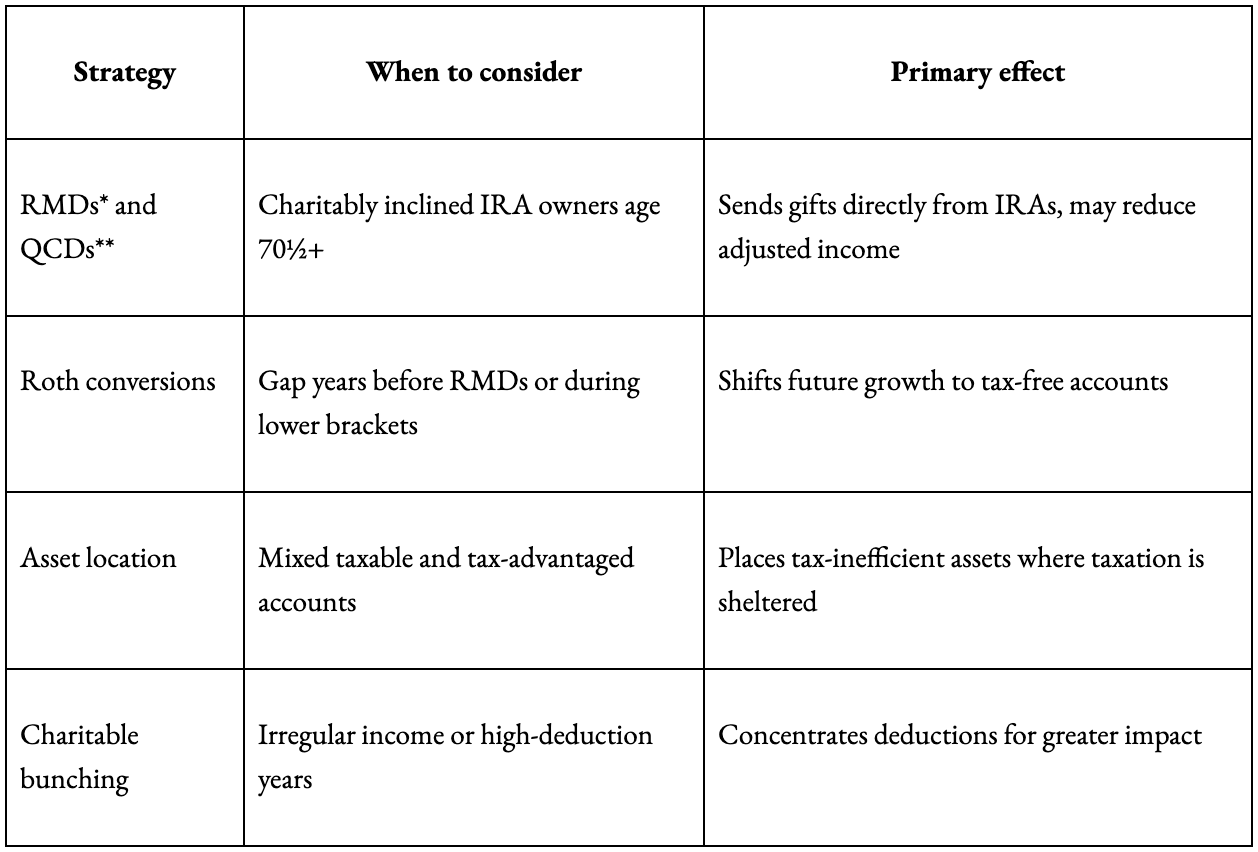

Tax-Efficient Cash Flow That Preserves Options

Cash-flow design affects flexibility, taxes, and Medicare premiums. Focus on withdrawal order, charitable tools, asset location, and the timing of advanced moves such as Roth conversions. Use modeling to see how each tactic changes lifetime taxes and optionality.

If turning plans into steps would help, request a retirement income review that maps withdrawal sequences, brackets, and giving strategies. Ask for a one-page summary you can revisit.

Trusts And Entities That Protect And Empower

Structures can clarify intent and reduce friction. Common tools include revocable trusts for administration, dynasty trusts for multigenerational protections, SLATs for indirect spousal access, ILITs for estate liquidity, and charitable vehicles such as donor-advised funds or charitable remainder trusts. Draft trustee powers and distribution standards that teach stewardship and phase in responsibility.

Family Governance: Passing Wisdom With The Wealth

Governance keeps wealth from becoming a blank check and turns values into habits that persist when circumstances change. And Good governance keeps money from becoming a source of stress at the very moments it is meant to help.

Set a simple rhythm for conversations, capture brief notes, and keep each agenda tied to what the family says matters most. Be clear about who decides what, when to pause, and how to bring in a neutral voice if things feel stuck. Letters of wishes give heart and context to the legalese, so trustees and heirs can act with confidence rather than guesswork. Share information in stages as adults are ready, celebrate small wins, and make space for questions that are easier to ask than to answer.

Investment Policy For Multi-Generation Capital

An investment policy is a calm voice when markets get loud. Define what the portfolio is here to do, how much risk feels acceptable, and the rules for rebalancing so decisions are steady on good days and hard ones. Keep a cash cushion for near-term needs, then let long-term assets work with global diversification and sensible inflation protection.

Focus on total return instead of chasing yield that can disappoint at the wrong time. Revisit the policy after life changes, not every headline, so the plan stays aligned with purpose.

Preparing Heirs: Skills, Access, Accountability

Preparation is an act of care: it reduces fear and builds trust. Start with low-stakes practice, like paying a month of bills together or reviewing a statement without jargon, then grow responsibilities as skills grow. Invite next-gen adults into selected meetings so they hear the questions, not just the answers.

Use incentives that encourage learning, work, and service while avoiding rules that feel like traps. Offer mentorship, give grace for honest mistakes, and keep the door open for help without judgment.

Real Estate And Business Succession Without The Drama

Properties and businesses often carry stories as well as numbers, which is why clear plans matter. Confirm titles and insurance, collect key contacts in one place, and keep a simple playbook so no one has to hunt for details under pressure. For a business, review the buy-sell, funding, and valuation method while everyone is on good terms, then outline who steps in if something unexpected happens.

Train successors with real tasks and timelines so confidence grows alongside responsibility. Bring your legal, tax, and advisory teams together periodically to keep documents and daily realities pointing in the same direction.

Philanthropy That Teaches Stewardship And Meets Tax Goals

Giving is a way to say what the family stands for. Choose a structure that fits your capacity, consider gifts of appreciated assets when the timing makes sense, and write a simple rubric for how grants get chosen. Invite younger voices to research causes and present proposals, then circle back to share what happened because of the gift.

Hold brief quarterly check-ins to keep generosity organized and meaningful rather than rushed. Track results with a few honest measures and a story or two, so purpose stays connected to people.

Legacy Documents: A Fast, Practical Checklist

Turn intentions into an actionable legacy plan by organizing the essentials. Use the checklist below to surface gaps, reduce friction, and keep documents aligned with your goals.

- Up-to-date will, revocable trust, powers of attorney, and health directives

- Verified beneficiary designations, including contingent and per-stirpes

- Asset inventory with titling, cost basis, and key contacts

- Investment Policy Statement, rebalancing rules, liquidity sleeve, and spending rate

- Trustee guidance or letter of wishes; distribution framework

- Philanthropy plan, grant rubric, and calendar

- Family meeting schedule, agenda template, and responsibilities

- Secure document vault with shared access and emergency instructions

Mark what is complete, then choose one priority to address this quarter. As items are finalized, note where each document lives and who is responsible, setting up a smooth transition into implementation in the next section.

Frequently Asked Questions About Legacy Building

What should be clarified first?

Purpose, people, and governance. Capture the vision, roles, and how decisions will be upheld, then align accounts and documents.

How do taxes fit?

Withdrawal order, Roth conversions, and QCDs can reduce drag while supporting lifestyle and giving. Modeling shows how small changes today protect flexibility over decades.

Which trusts help most?

Revocable trusts ease administration, dynasty trusts extend protections, SLATs and ILITs address access and liquidity. The right tool is the one that advances your mission without unnecessary complexity.

How do we avoid entitlement?

Education, phased transparency, and incentive provisions. Tie distributions to milestones or service so stewardship grows with responsibility.

What belongs in our investing rules?

A spending policy, risk budgets, rebalancing bands, and a plan to refill liquidity. Link rules to time horizon so near-term needs do not crowd out long-term aims.

How often should a family meet?

At least annually, with check-ins around life events. Use agendas that link decisions to the mission and keep minutes with next steps to maintain momentum.

Next steps: put your plan in motion?

Legacy planning works best when intention becomes coordinated action. If a fresh look would help, contact the office for a focused session that prioritizes steps, aligns legal and tax inputs, and creates a simple timeline that keeps your enduring legacy both principled and practical.

*RMD: required minimum distribution

**QCD: qualified charitable distribution