High-value collections tell a story, often across decades of discerning choices and careful stewardship. Translating that story into an enduring, effective estate plan requires more than a simple will. It calls for a framework that respects authenticity, market cycles, and family wishes while navigating valuation and tax complexity. This article outlines a clear approach for planning around art, wine, rare autos, and other alternative assets, so your legacy can remain intact long after a sale, gift, or bequest.

Key Takeaways

A thoughtful plan for art, wine, and similar assets can accomplish two things at once. It can help preserve meaning while managing liquidity, taxes, and control. The points below preview what this guide covers and how to apply it.

Illiquid collections introduce appraisals, storage, insurance, and authenticity documentation that ordinary portfolios do not.

Ownership structures, such as LLCs and purpose-built trusts, can streamline governance and distributions while containing fiduciary risk.

Transfer pathways, lifetime or testamentary, can involve trade-offs in tax treatment, control, and liquidity, which can be mapped and compared.

Charitable tools, including outright gifts, promised gifts, and split-interest trusts, may align impact objectives with tax efficiency when structured carefully.

A practical, repeatable process, inventory, valuation cadence, custodial agreements, and family governance, reduces friction during transitions.

Used together, these steps can help protect both financial value and the narrative value of a collection. For a tailored roadmap that fits your family’s goals, contact the office.

Why Hard-to-Value Collections Need a Different Playbook

Illiquid assets behave differently from marketable securities. Pricing can be episodic, data is uneven, and transaction costs can vary widely. Estate plans that assume daily liquidity are often ill-fitted in light of these realities.

Valuation, Provenance, and Appraisal Cadence

For estate and gift purposes, defendable valuation is essential. Qualified appraisers, current condition reports, and complete provenance files support tax filings and fiduciary decisions. Creating a cadence, for example, formal appraisals at set intervals and targeted updates after notable market events, can prevent valuation gaps that complicate transfers or charitable deductions.

Concentration Risk and Liquidity Planning

Collections can dominate a balance sheet. When estate taxes or equalization needs arise, forced sales may depress outcomes. A liquidity plan, which can include maintained credit lines, dedicated cash reserves, or staged dispositions, gives fiduciaries options. Aligning sale windows with the market’s calendar, major auctions and seasonal demand, may improve execution quality.

Family Dynamics and Stewardship

Not every heir wants custodial responsibilities. Some want to curate, others prefer liquidity or shared access. Early conversations, letters of wishes, and clear decision rights can help reduce conflict and ambiguity. Consider how successors will address conservation, storage, and insurance, along with how they will interpret any “no-sale” preferences over time.

Building an Effective Ownership Structure

The appropriate entity or trust can simplify administration, clarify control, and position the collection for smoother transfers. The structure should align with intent, income potential, and desired privacy.

LLCs and Series LLCs for Collections

An LLC can hold title, centralize bills and insurance, and provide for voting and transfer restrictions. Operating agreements can assign curatorial authority, loan policies to institutions, and sale thresholds. Where permitted, a series LLC can separate sub-portfolios, such as Old Masters and contemporary or Burgundy and Napa, each with distinct accounting and rights. Be thoughtful about valuing interests in the LLC, discounts for lack of control or marketability must be well supported with a qualified appraisal.

Trusts for Specialty Assets

Irrevocable trusts, grantor or non-grantor, can own entity interests or assets directly. Directed trusts allow investment and distribution decisions to rest with designated parties, which is helpful when a corporate trustee prefers not to hold physical wine or art. Purpose clauses, display and conservation standards, and permitted sale conditions can be written with enough flexibility to adapt as markets, storage costs, and family preferences evolve.

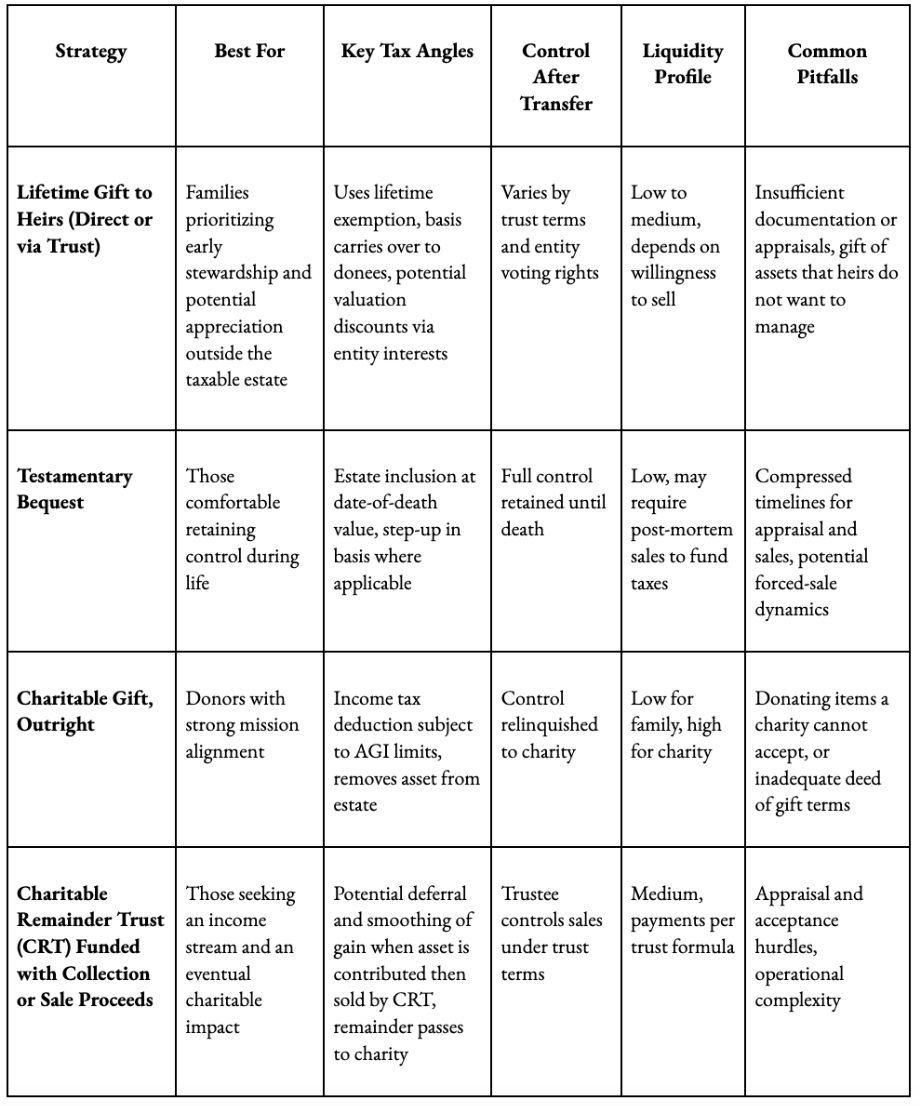

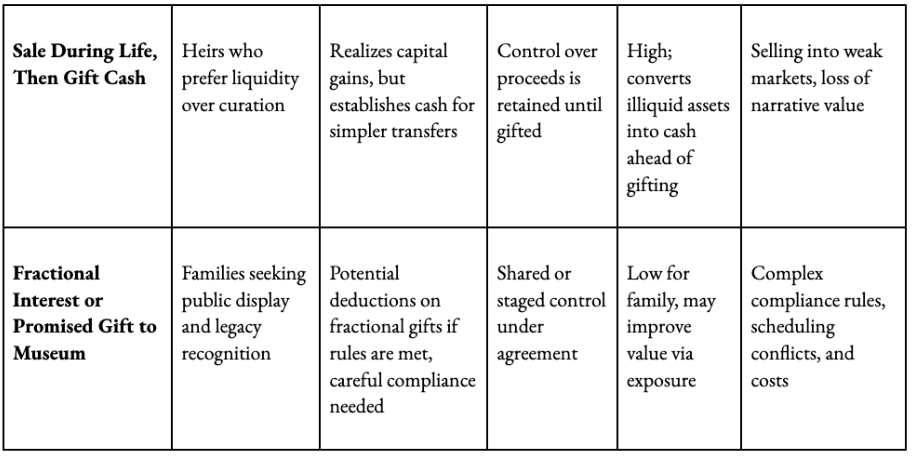

Comparing Transfer Pathways for Illiquid Collections

Each transfer path leads to a different outcome. Use the table below to see how common strategies may align with control, liquidity, and tax considerations.No single method is universally superior. A blended approach, for example, entity ownership now with a testamentary plan that bifurcates “keep forever” pieces from “sell to equalize” pieces, can align family sentiment with financial realities.

The Illiquid Asset Checklist for High-Net-Worth Estate Planning

A resilient plan rests on basics done well. Gather the following pieces now to help support any strategy and keep surprises to a minimum.

Create a complete inventory, images, purchase history, provenance, and location data, with secure digital backups.

Formalize storage and custody, climate specs, bonded warehouse or vault terms, and emergency procedures.

Update insurance, confirm agreed value versus market value policies, exclusions, and transit coverage.

Establish an appraisal plan, a qualified appraiser list, frequency, and event-driven triggers.

Set governance, operating agreement, or trust provisions for loans, sales, and dispute resolution.

Prebuild liquidity, dedicated reserves, credit facility, or staged sale plan aligned to market calendars.

Map tax reporting, gift and estate filings, charitable substantiation, and export or cultural property rules.

Clarify succession, designate successor fiduciaries, curator or consultant relationships, and family meeting cadence.

This practical checklist can help you lay the groundwork to prevent costly detours. With these pieces in place, you, your heirs, financial professionals, and other advisors can make confident decisions.

Working With Institutions, Dealers, and Fiduciaries

A network of aligned partners adds resilience. Define roles up front and document expectations to avoid surprises during time-sensitive events.

Museums and Charities: From Loan to Legacy

Loans can showcase a collection, enhance provenance, and deepen relationships that lead to promised gifts. Loan agreements should specify shipping, installation, insurance, and attribution. For charitable transfers, confirm acceptance criteria early, collection policies, deaccession rules, and whether the organization can maintain specialized storage or conservation.

Dealers, Auction Houses, and Market Windows

Dispositions can benefit from competitive tension. Consignment agreements should address reserves, fees, photography, and timing. Consider geographic venues and sale seasons, since demand for specific categories is cyclical. A right of first offer for heirs or the holding entity can balance family access with market execution.

Insurance, Storage, and Custody

Insurance coverage for your illiquid assets and collections should reflect the realities of ownership and management. In the instance of wine, for example, bonded storage, lot tracking, and temperature monitoring are essential. For art, condition reports before and after transit, crate specifications, and courier protocols can help protect value. Periodic vendor reviews can also help keep terms current as the collection evolves.

Governance That Reduces Conflict

Documents can set the tone, but family culture and communication sustains it. Governance that is clear, succinct, and repeatable can help heirs respect each other, the collection, and the legacy.

Decision Rights and Communication

Spell out who decides what, sale thresholds, acquisition rules if the entity remains active, and how proceeds are allocated. Schedule standing family meetings, share coherent reporting, and keep minutes. A short, values-driven letter of wishes can guide trustees without binding them to rigid instructions.

Equalization and Fairness

When only some heirs want to curate, fairness mechanisms matter. Equalization can be addressed with life insurance owned outside the taxable estate, staged sales with proceeds balancing other inheritances, or a buy-sell right that allows interested heirs to acquire works at a documented fair price. Transparency can help reduce conflict and litigation risk.

Frequently Asked Questions About High-Net-Worth Estate Strategies For Illiquid Collections

Below are concise answers to common questions that arise when planning around art, wine, and other specialty assets in high-net-worth estates. Use them as a starting point, then get in touch with the office for guidance tailored to your situation.

How often should a collection be appraised for planning purposes?

A practical cadence is every one to three years, with event-driven updates after significant acquisitions, conservation work, market shifts, or before large gifts and sales. The goal is a defendable record that aligns with tax, insurance, and fiduciary needs.

Can a corporate trustee hold physical wine or art?

Policies vary. Some corporate trustees prefer to hold entity interests rather than the assets directly, which is why an LLC owned by the trust can be efficient. Directed trust structures can further allocate responsibilities to specialized advisors.

Are fractional gifts to museums still practical?

They can be, when carefully structured. Compliance, use requirements, and valuation rules are exacting, so early coordination with counsel and the institution prevents unpleasant surprises.

What if heirs disagree about selling versus keeping?

Anticipate this in governing documents. Set sale thresholds, curator rights, and a dispute ladder, for example, mediation before any petition to a court. Equalization mechanisms can reduce zero-sum choices.

How do export and cultural property rules affect sales?

Certain works and artifacts may be subject to export controls or cultural patrimony laws. Vendor diligence and counsel experienced in cross-border transactions can help ensure lawful, timely transfers.

Charting Next Steps for High-Net-Worth Estate Planning

Fine art, wine, and other illiquid collections deserve plans as distinctive as the assets themselves. To effectively incorporate these illiquid assets into your high-net-worth estate plan, start with documentation and governance, then select structures and transfer pathways that match your family’s preferences and the market reality for each category. A strong plan should do more than cover taxes; it can preserve narrative value, protect relationships, and give future decision makers practical room to maneuver.

Get in touch with the office today to schedule a meeting to discuss your legacy plans and how to incorporate your high-value illiquid assets and collections. Together, we can scope a valuation cadence, align the appropriate entity or trust structure, frame museum or charitable options, and model the liquidity needed for taxes and fairness among heirs. A brief conversation can help you confirm priorities, set timelines, and coordinate your entire advisory team so the collection reflects both your taste and your intent for the next generation.