In retirement, inflation shows up in practical ways: groceries, prescription costs, insurance premiums, home repairs, and property taxes. Even gradual price increases can weaken purchasing power over time, especially when your income is fixed or only partly adjustable.

The good news is that planning for inflation does not need to be complicated. It does need to be purposeful.

This guide explains how rising costs can affect your retirement income, how Social Security cost-of-living adjustments fit into the picture, and which planning strategies may help protect your lifestyle over time.

Key Points to Keep in Mind

Inflation can affect nearly every part of a retirement plan, from day-to-day spending to long-term investment decisions. Understanding the basics can help you make more informed choices.

Here are the main ideas to know:

Inflation reduces purchasing power over time. Even moderate increases can create a meaningful gap over a long retirement.

Not all income adjusts with inflation. Social Security includes COLAs, but many pensions and annuities pay a fixed amount.

Healthcare deserves separate attention. Medical costs and long-term care expenses may rise faster than general inflation.

Your portfolio can help offset inflation risk. Growth assets, inflation-linked bonds, and cash reserves can each play a role.

Withdrawal flexibility matters. Guardrails, bucket strategies, and annual reviews can help your income plan adapt.

Small adjustments can help. You may not need a major lifestyle overhaul if your plan is reviewed and updated regularly.

With those fundamentals in mind, let’s look at the planning decisions that can help you prepare for inflation in retirement.

Why Rising Prices Matter After You Retire

Inflation means your money buys less as time passes. A 2.5% to 3.0% inflation rate may sound modest, but over 10, 20, or 30 years, it can significantly increase the income needed to maintain the same lifestyle. A shorter period of higher inflation, such as 5% for several years, can be even more disruptive.

The objective is not to guess future inflation perfectly. It is to build a retirement plan that can respond. That means incorporating inflation into your spending assumptions, income projections, portfolio design, and annual review process.

Which Inflation Gauge Should Retirees Watch?

You may hear several versions of the Consumer Price Index, or CPI, mentioned in the news. Each one measures inflation in a slightly different way.

CPI-U: A broad inflation measure for all urban consumers and one of the most commonly cited inflation gauges.

CPI-W: The measure used to calculate Social Security cost-of-living adjustments. It reflects urban wage earners and clerical workers.

CPI-E: An experimental measure focused on older Americans, with more weight on costs such as healthcare and housing.

For planning purposes, CPI-U provides broad context, CPI-W matters for Social Security COLAs, and CPI-E can be a useful reference for retiree-specific expenses.

Where Social Security COLAs Fit In

Social Security’s annual cost-of-living adjustment is intended to help benefits keep pace with inflation. Still, COLAs do not always match your personal spending experience. Healthcare, insurance, housing, and taxes may rise differently than the official measure.

It can help to think about retirement income in two layers:

A dependable income base: Social Security, pension income, inflation-adjusted annuities, or other reliable sources.

A flexible income layer: Withdrawals from savings, investments, and other assets that can be adjusted as conditions change.

When COLAs do not fully offset rising expenses, your portfolio may need to help fill the gap. In years when COLAs are stronger, you may be able to reduce pressure on investment withdrawals.

Understanding Fixed Versus Inflation-Linked Income

Some pensions and annuities include inflation adjustments. Many do not. A fixed payment may feel reliable early in retirement, but its purchasing power can decline as prices rise. Inflation-adjusted income may offer stronger long-term protection, though it can start lower or cost more upfront.

Other income sources, such as rental income, consulting income, or business income, may adjust somewhat with inflation. They can also fluctuate.

When evaluating income sources, consider two questions:

How reliable is this income?

Can it increase when costs rise?

This helps clarify how much of your lifestyle is covered by steady income and how much depends on your investment portfolio.

Planning for Healthcare and Long-Term Care Costs

Healthcare costs can rise faster and less predictably than general inflation. Medicare premiums, prescription drug costs, supplemental coverage, and out-of-pocket expenses may all change over time. Long-term care costs can add another layer of uncertainty.

Consider these planning steps:

Review coverage each year. During Medicare open enrollment, compare premiums, provider networks, prescription coverage, and plan changes.

Use separate healthcare assumptions. Many retirement plans model healthcare inflation at a higher rate than general expenses.

Address long-term care early. This may include setting aside assets, evaluating insurance options, or identifying home equity as a possible contingency.

A thoughtful plan can help reduce the chance that rising medical costs disrupt your broader retirement strategy.

Investment Approaches That May Help With Inflation

Inflation risk cannot be removed completely, but your portfolio can be designed to support near-term spending, provide growth potential, and remain flexible as conditions change.

The right mix depends on your needs, risk tolerance, tax situation, and time horizon.

Common Portfolio Tools

Short-duration bonds and cash-like investments: Help support near-term spending needs and stability.

Treasury Inflation-Protected Securities, or TIPS: Bonds designed to adjust principal with inflation.

I Bonds: U.S. savings bonds with an inflation-linked component.

Equities, including dividend growers: May provide long-term growth potential.

Real assets: Real estate, infrastructure, or commodities exposure may help diversify inflation risk.

Segmenting Assets by Time Horizon

A bucket strategy organizes assets by when you expect to use them.

Near-term bucket, 0 to 3 years: Cash, Treasury bills, and short-term bonds for immediate spending.

Intermediate bucket, 3 to 7 years: High-quality bonds or income-focused assets for medium-term needs.

Long-term bucket, 7+ years: Growth-oriented assets intended to help outpace inflation over time.

This structure can help retirees maintain accessible funds for near-term needs while giving long-term assets more time to work.

Pairing Reliable Income With Growth Potential

Another approach is to identify the reliable income needed to cover essential expenses first. That may include Social Security, pensions, annuities, or other dependable income sources.

The remaining portfolio can then be positioned for growth and flexibility. The income base supports core needs, while the growth portion helps the plan respond to inflation and fund discretionary goals over time.

Using Flexible Withdrawal Guardrails

A dynamic withdrawal strategy adjusts spending within pre-set limits. Instead of increasing withdrawals by the same percentage each year, guardrails allow withdrawals to respond to market performance, inflation, and portfolio health.

In strong markets, withdrawals may increase modestly. During difficult markets or high-inflation periods, withdrawals may stay level or decrease slightly. The goal is to adapt thoughtfully rather than react emotionally.

Stress-Testing Your Retirement Income

Stress-testing helps you see how your plan may respond under different conditions. At minimum, consider reviewing:

A baseline inflation assumption of about 2.5% to 3.0%.

A higher inflation scenario of about 5% lasting 3 to 5 years.

Then evaluate how those assumptions affect portfolio longevity, withdrawal rates, and essential income coverage.

If most essential expenses are covered by COLA-linked or inflation-adjusted income, your plan may be better positioned. If not, you may need to revisit spending, withdrawal timing, or inflation-sensitive income options.

Adjusting Without Overreacting

Inflation does not always require major lifestyle changes. Often, small, steady adjustments can make a meaningful difference.

Be strategic with large purchases. Consider delaying or spacing out discretionary spending.

Coordinate withdrawals. Use taxable, tax-deferred, and Roth accounts thoughtfully.

Review your plan regularly. Update assumptions annually, or sooner after major market or inflation changes.

A disciplined review process can help keep decisions manageable and aligned with your long-term goals.

Using Housing as Part of the Inflation Plan

Housing can play a major role in retirement inflation planning. Downsizing may reduce taxes, insurance, maintenance, and utility costs. A home-equity line of credit may provide flexibility during market downturns or unexpected expenses.

For those planning to age in place, maintaining a cash reserve can be especially helpful. A reserve equal to one to three years of planned withdrawals may help reduce the need to sell long-term assets during unfavorable markets.

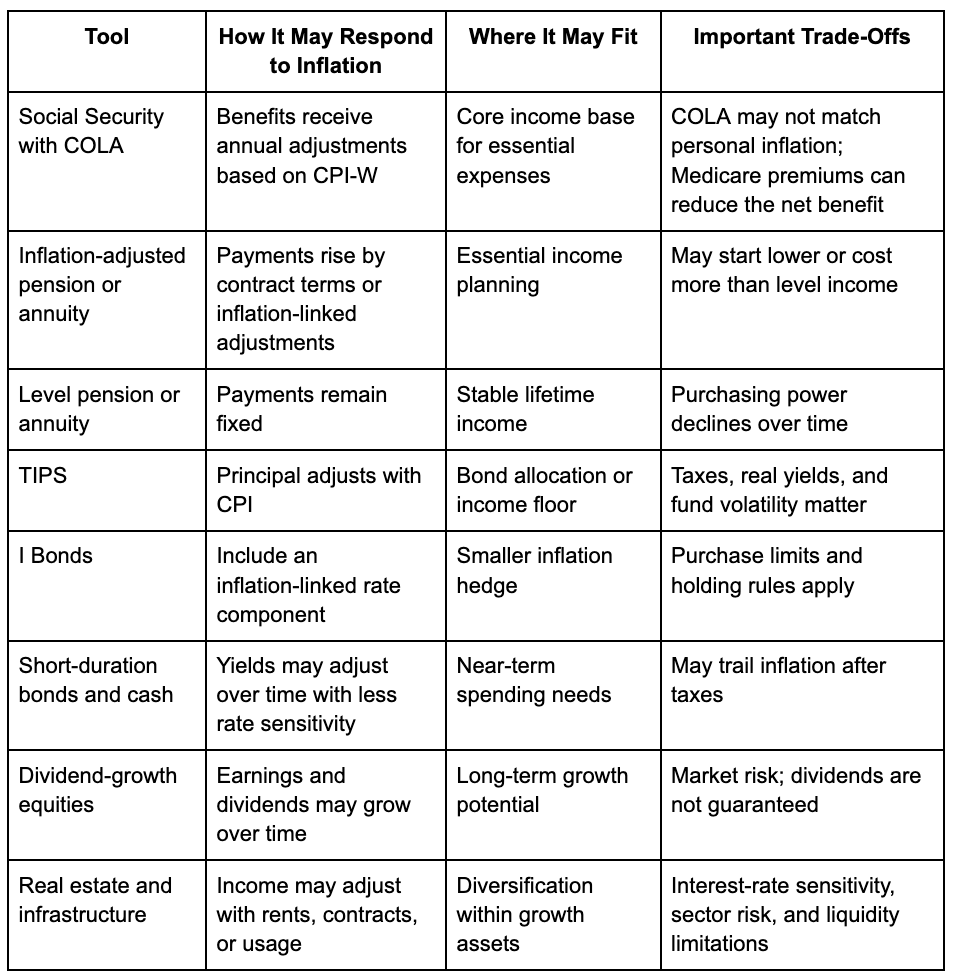

Inflation Planning Tools at a Glance

The table below offers a high-level look at common tools that may help address inflation in retirement.

These tools are not one-size-fits-all. Their value depends on how they work together within your broader retirement income plan.

Common Questions About Inflation and Retirement

What inflation rate should retirees use in planning?

A practical starting point is 2.5% to 3.0% for general expenses, paired with a higher stress-test assumption near 5% for several years. Healthcare may need a separate, higher assumption.

Does cash protect retirees from inflation?

Cash can provide stability and support near-term spending, but it can lose purchasing power when inflation is higher than short-term yields. Many retirees balance cash reserves with investments that offer growth or inflation adjustment potential.

Do Social Security COLAs cover inflation completely?

COLAs help, but they may not fully match your personal expenses. Healthcare premiums and other retiree costs can absorb part of the increase.

Are TIPS or I Bonds right for every retiree?

Not always. TIPS and I Bonds can be useful, but they should fit your tax situation, liquidity needs, account structure, and broader investment plan.

Which withdrawal strategy works best when inflation rises?

Dynamic withdrawal strategies, such as guardrails, can help spending adjust to market and inflation conditions. Bucket strategies and reliable-income-plus-growth approaches can also provide helpful structure.

How often should retirees revisit inflation assumptions?

A yearly review is a good starting point. Additional reviews may be helpful after major market changes, inflation surprises, healthcare changes, or significant life events.

How does housing fit into inflation planning?

Housing affects both lifestyle and cash flow. Downsizing, home equity, maintenance planning, and aging-in-place costs should all be considered as part of your retirement strategy.

How to Keep Your Retirement Plan Prepared for Inflation

Inflation will always be part of retirement planning, but it does not have to control your financial future. The key is to understand your income sources, know which expenses may rise fastest, maintain a flexible withdrawal strategy, and review your plan regularly.

A strong retirement plan should help you:

Cover essential expenses with reliable income where possible.

Keep enough liquidity for near-term needs.

Maintain growth potential for long-term purchasing power.

Plan separately for healthcare and long-term care costs.

Adjust spending and withdrawals as conditions change.

If you would like to understand how inflation could affect your retirement income, connect with WealthPartners to review your assumptions, stress-test your strategy, and build a plan for the lifestyle you have worked hard to enjoy.