Losing a spouse reshapes daily life and financial routines at once. In the midst of paperwork and difficult choices, Social Security surviving spouse benefits can provide steadier footing, yet the rules behind eligibility, amounts, and timing are not always intuitive.

This brief guide clarifies who may qualify, how payments are calculated from a late spouse’s work record, and when it could make sense to claim or switch. The goal is to help you coordinate survivor benefits with retirement income, taxes, and Medicare so decisions feel measured rather than rushed. If a personalized walkthrough would help, contact the office to review options and build a simple timeline.

Key Takeaways

Below is a concise overview of what matters most before taking next steps. Review these points to frame the decisions ahead, then move into the details below.

- Eligibility commonly begins at 60; it can begin at 50 if disabled, or at any age with a child-in-care.

- The payment is tied to the deceased spouse’s Primary Insurance Amount and reflects early filing or delayed credits on that record.

- Many households start survivor benefits first, then switch to their own retirement benefit later if it will be higher.

- Working before survivor full retirement age can trigger the earnings test; taxation is a separate calculation.

- Modeling survivor benefits alongside withdrawals, Medicare, and RMD timing can clarify when to claim and how to coordinate income.

Bottom line: Align eligibility, amount, and timing with the broader retirement income and tax plan, then reach out to the office to review options.

What Survivor Benefits Are, And Who Qualifies

Survivor benefits are monthly Social Security payments based on a deceased spouse’s work record. When the deceased earned enough credits, a surviving spouse may receive a benefit that reflects what the worker received or was entitled to receive at death.

Many widows and widowers qualify beginning at age 60, or at 50 when disabled. Eligibility can also apply at any age when caring for a qualifying child who is under 16 or disabled. Survivor rules are separate from standard spousal rules, which allows strategic coordination with a personal retirement benefit.

Surviving Divorced Spouse Rules

A surviving divorced spouse may qualify when the prior marriage lasted at least ten years and other criteria are met. Current marital status and the timing of remarriage can affect eligibility, so it is important to confirm dates and documentation before filing.

How The Amount Is Calculated

The anchor is the deceased worker’s Primary Insurance Amount, which is based on lifetime indexed earnings. If the worker filed early, the survivor amount may be lower; if the worker delayed beyond full retirement age and earned delayed retirement credits, those credits can increase the survivor payment. A specialized widow(er)’s limit can constrain the final amount, and annual cost-of-living adjustments generally flow through to survivor payments.

When To Claim, And Why Timing Matters

Survivor benefits can begin at 60, though filing before survivor full retirement age reduces the monthly amount. Survivor full retirement age may differ from the age that applies to a personal retirement benefit, so verify both before deciding.

Waiting beyond survivor full retirement age rarely increases the payment further because any delayed credits earned by the deceased are already included. The goal is to balance current cash needs with long-term income sustainability.

Coordinating Survivor Benefits With A Personal Retirement Benefit

Social Security pays one combined amount rather than two full benefits at once. Often this is structured as a personal retirement benefit with a survivor top-up to reach the higher figure. A common approach is to start survivor benefits first and switch later to a personal retirement benefit if it will be larger at age 70.

If the personal benefit already exceeds the survivor amount, relying on the personal benefit may be appropriate. A brief comparison can confirm whether a short period on survivor benefits before switching creates any advantage.

Integrating Survivor Benefits With Portfolio And Tax Strategy

Coordinating survivor benefits with Roth conversions, pension elections, annuity income, and required minimum distributions can help smooth cash flow and manage lifetime taxes. Sequencing matters because adding or reducing taxable income in certain years can affect how much of the Social Security benefit is taxable and can influence Medicare premiums.

Special Situations That Change The Math

Remarriage before age 60 generally ends eligibility on the prior spouse’s record; remarriage at 60 or later usually preserves eligibility. If a later marriage ends, eligibility may be reinstated, subject to rules in effect at that time. When caring for a child who is under 16 or disabled, survivor benefits may be available regardless of age, though family maximums and coordination rules can apply.

If receiving a pension from employment not covered by Social Security, the Government Pension Offset may reduce survivor payments, and the Windfall Elimination Provision can indirectly affect the calculation through the worker’s own record.

If You Are Working, Know The Earnings Test And Taxes

Earnings above the annual limit before survivor full retirement age can lead to temporary withholding under the earnings test. Withheld amounts are not lost, yet near-term cash flow can be tighter until adjustments occur at full retirement age.

Taxes are separate from the earnings test; depending on combined income, up to 85 percent of Social Security benefits can be taxable. Coordinating withdrawals and charitable strategies may help manage the tax impact over time.

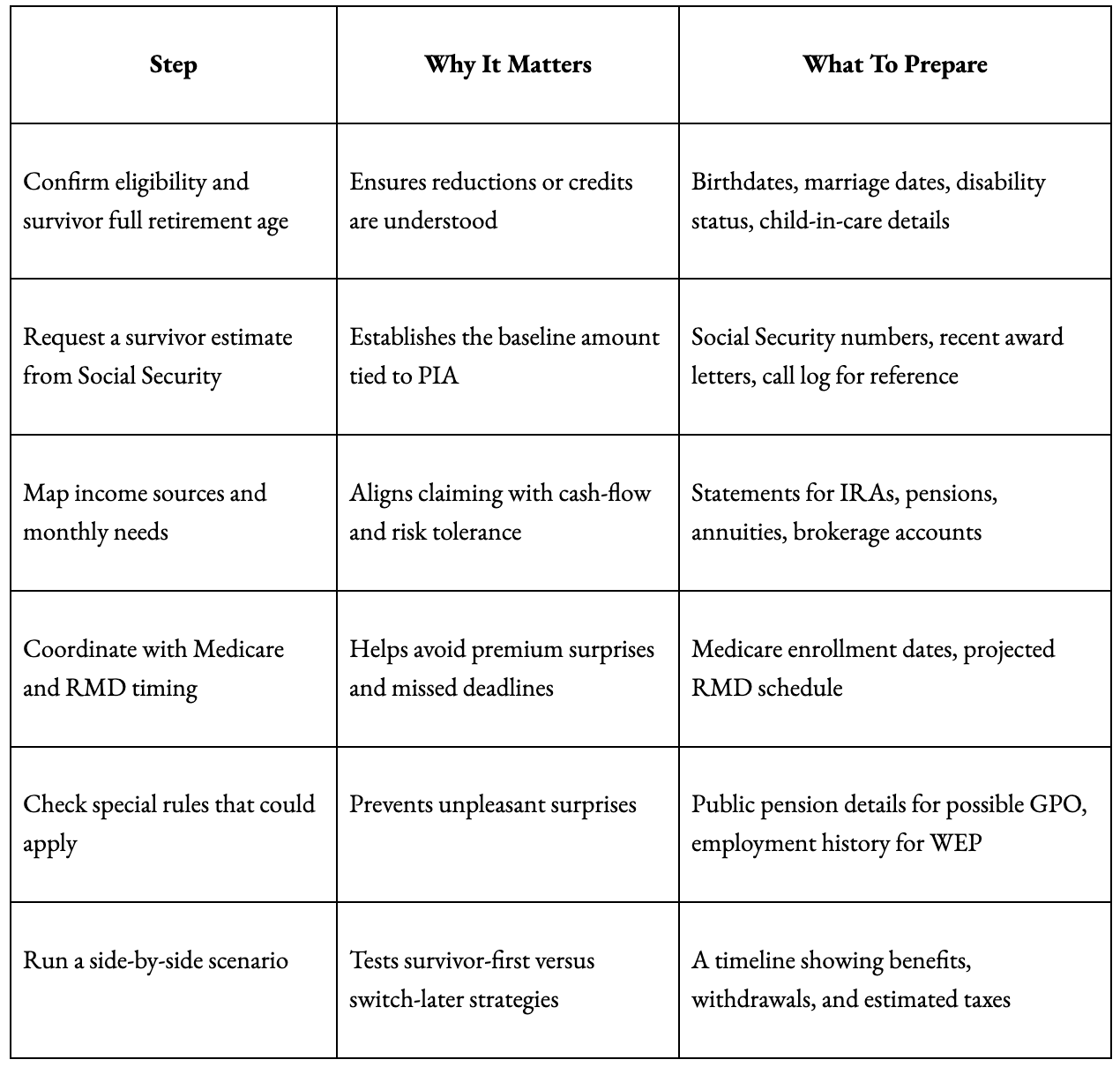

Action Table: Organize Key Steps And Dates

Before filing, it helps to organize documents and deadlines and to request official figures. Use the table below to create a simple plan, then follow with a brief strategy session to integrate income sources.

This table is a starting point. A personalized model can show how survivor benefits interact with withdrawals, taxes, and premiums across several years. For clarity on sequencing and cash flow, contact the office.

Frequently Asked Questions About Common Questions About Surviving Spouse Benefits

This brief Q&A addresses questions that tend to come up during the first conversation. For nuances unique to your situation, get in touch with the office.

Can survivor benefits and a personal benefit be received at the same time?

You may qualify for both, yet Social Security generally pays the higher of the two as a single amount. Some start survivor benefits first, then switch to a personal benefit later.

Does waiting past survivor full retirement age increase the survivor benefit?

Typically it does not. When the deceased earned delayed retirement credits, those are usually already reflected in the survivor benefit.

Will remarriage end survivor benefits?

Remarriage before age 60 generally ends eligibility on the prior spouse’s record. Remarriage at 60 or later typically preserves eligibility.

How does working affect payments before survivor full retirement age?

Earnings above the annual limit can lead to temporary withholding under the earnings test. Adjustments at full retirement age account for prior reductions, yet near-term cash flow can be affected.

Are survivor benefits taxable?

Depending on combined income, up to 85 percent of Social Security benefits can be taxable. Coordinating survivor benefits with withdrawal sequencing can help manage taxation over time.

What about the Government Pension Offset and the Windfall Elimination Provision?

The Government Pension Offset may reduce survivor benefits when a non-covered pension is involved. The Windfall Elimination Provision affects a worker’s own benefit and can influence survivor calculations indirectly.

Can a surviving divorced spouse receive survivor benefits?

Yes, when the marriage lasted at least ten years and other eligibility rules are met. Proper documentation and attention to timing are essential.

Can a survivor switch later to a personal benefit?

Often yes. Starting survivor benefits and switching later can be beneficial when the personal benefit at 70 will be higher.

Do cost-of-living adjustments apply to survivor benefits?

In general, annual cost-of-living adjustments flow through to survivor payments and help maintain purchasing power.

What should be brought to an appointment?

Bring identification, the deceased spouse’s information, marriage and death certificates, and Social Security correspondence. If meeting with a financial professional, include recent account statements to model how survivor benefits fit into the plan.

Are survivor benefits taxed differently once RMDs begin?

Required minimum distributions increase adjusted gross income and can cause more of the Social Security benefit to be taxable. A coordinated plan can reduce surprises.

Plan Your Next Steps

Survivor benefits can stabilize income when coordinated carefully with the broader retirement and tax picture. Eligibility rules, calculation details, and claim timing all shape long-term outcomes, and special situations such as remarriage, children-in-care, GPO, WEP, and working before survivor full retirement age can change the decision tree. If a time-sensitive choice is ahead, contact the office for a side-by-side timeline that coordinates survivor benefits with other income sources, taxes, and Medicare milestones.